马耳他是欧洲最大和世界上第六大的海上注册中心。它尤其是欧洲最大的娱乐游艇和超级游艇登记中心之一。

马耳他海事行业的成功,乃至休闲游艇的成功基于两大因素:

- 租赁的休闲游艇和超级游艇在欧盟水域内使用基础上进行财政计划的可能性 马耳他对休闲游艇的长期租赁提供有针对性的指南。指南提出在租赁期间,增值税只会在船只在欧盟范围内的使用基础上征收,在欧盟范围外的使用免征收增值税。此指引在2019年3月正式公布,取代2005年的旧指引,于2018年11月生效。最新的指引反映了马耳他在该行业的经验,欧盟的发展和实例操作。根据预期的操作,使用游艇用作财政计划和实际用途,一些型号可以使用。有利的租赁设立是指马耳他公司将休闲游艇出租给一个无需纳税的自然人或实体,可从该指南中得益:增值税仅对承租者在欧盟范围内游艇的实际使用的基础上征收。

- 国旗声望以及注册口碑。马耳他对注册和解除船舶登记提供简单直接的手续,包括基于融资手段申请和解除抵押贷款,高竞争力的登记和续期费用, 最低技术要求便于休闲游艇船主自由设计游艇和全天候24小时处理紧急事务的服务。

船国旗督查确保船舶遵守国际标准,对马耳他船只的船长,高级船员和船只服务员的国籍没有任何限制。

马耳他是欧洲最大和世界上第六大的海上注册中心。它尤其是欧洲最大的娱乐游艇和超级游艇登记中心之一。

马耳他海事行业的成功,乃至休闲游艇的成功基于两大因素:

- 租赁的休闲游艇和超级游艇在欧盟水域内使用基础上进行财政计划的可能性 马耳他对休闲游艇的长期租赁提供有针对性的指南。指南提出在租赁期间,增值税只会在船只在欧盟范围内的使用基础上征收,在欧盟范围外的使用免征收增值税。此指引在2019年3月正式公布,取代2005年的旧指引,于2018年11月生效。最新的指引反映了马耳他在该行业的经验,欧盟的发展和实例操作。根据预期的操作,使用游艇用作财政计划和实际用途,一些型号可以使用。有利的租赁设立是指马耳他公司将休闲游艇出租给一个无需纳税的自然人或实体,可从该指南中得益:增值税仅对承租者在欧盟范围内游艇的实际使用的基础上征收。

- 国旗声望以及注册口碑。马耳他对注册和解除船舶登记提供简单直接的手续,包括基于融资手段申请和解除抵押贷款,高竞争力的登记和续期费用, 最低技术要求便于休闲游艇船主自由设计游艇和全天候24小时处理紧急事务的服务。

船国旗督查确保船舶遵守国际标准,对马耳他船只的船长,高级船员和船只服务员的国籍没有任何限制。

国家特色

| 世界性指标: 欧洲最大的注册中心 世界排名第6位 |

休闲游艇租赁增值税: 视乎在欧盟水域内的实际和有效使用上征收 |

| 注册总吨位: 超过5700万 |

货船注册: 48小时 |

| 注册船数: 超过11,000只 |

访问&应急: 24小时注册服务 |

| |

|

法律基础

马耳他针对游艇租赁的增值税对应手段源于欧盟增值税指令, 马耳他增值税法案(马耳他法第406章)和2019年3月发表的马耳他休闲游艇租赁指引。

使用的规则区分于:

- 短期租赁:不超过90天的游艇租赁

- 长期租赁:超过90天的游艇租赁

对于短期租赁,马耳他增值税在承租人开始自由支配游艇起开始征收。

对于长期租赁,增值税的征收取决于该服务的提供地是否被认为发生在马耳他:

- 出租者是否在马耳他;和

- 承租人是否在马耳他自由支配使用游艇

在马耳他长期租赁的情况下,指引说明了增值税被征收的条件:仅征收休闲游艇在欧盟水域内使用的增值税,在国际海域和欧盟水域外的使用不征收增值税。这是基于欧盟增值税指令,文章59a:成员国只对发生在欧盟范围内使用和享受的服务(包括休闲游艇的租赁)征收增值税。

如果实际有效使用游艇是在欧盟以外的地方以及遵循准则规定,提供租赁游艇的地点可被视为在欧盟领海之外。

在租赁期间,承租人需要向出租人提供记录来决定实际使用和享受游艇是否发生在欧盟水域内/外。

考虑到游艇租赁的费用一般都是提前交付,因此提供了额外的指引:

- 一种基于初步比率的计算应付增征税的方法:第一次增值税退税和增值税支付的初步比率;和

- 一种调整机制,最终确保整个租赁期间,增值税的支付反映了承租人在欧盟 海内使用和享受游艇的实际情况

优势

- 马耳他增值税:只在欧盟领海内使用产生

- 18%增值税率-欧盟海港-国中最低

- 针对在欧盟范围内实际使用产生应缴增值税的调整机制

- 反映欧盟发展和实践的指南

资质

- 出租者:一间在马耳他注册增值税号的公司

- 承租者:自然人或者实体承租游艇作为私人使用

- 租赁:长期,超过90天

- 游艇:承租者可在马耳他自由支配使用

- 记录:保留船只在欧盟范围内使用的记录,以反映增值缴纳情况

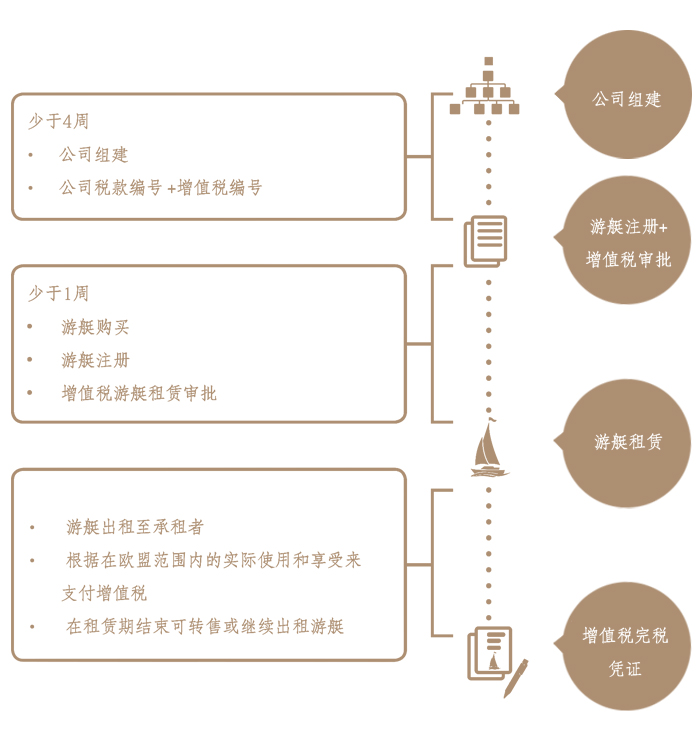

流程及时间

为什么与我们合作