Value added tax (VAT) is a consumption tax on goods and services bought and sold for use or consumption within the EU VAT area. VAT must be paid to the revenue authorities by the seller of the goods/ provider of service whilst the charge is borne by the consumer. In the context of use of yachts in the EU and their free circulation in EU territorial waters, VAT implications arise for yachts purchased in or formally imported in the EU. Different rules apply depending on whether the yacht shall be used privately or for commercial purposes. A number of models may be used depending on the intended operations and use of the yacht for fiscal planning and effectiveness. Beneficial lease set-ups wherein entities lease a yacht to a nontaxable person or entity offer attractive fiscal proposals. The most adequate model for the particular situation depends on the specifications of the yacht and the intended use.

Value added tax (VAT) is a consumption tax on goods and services bought and sold for use or consumption within the EU VAT area. VAT must be paid to the revenue authorities by the seller of the goods/ provider of service whilst the charge is borne by the consumer. In the context of use of yachts in the EU and their free circulation in EU territorial waters, VAT implications arise for yachts purchased in or formally imported in the EU. Different rules apply depending on whether the yacht shall be used privately or for commercial purposes. A number of models may be used depending on the intended operations and use of the yacht for fiscal planning and effectiveness. Beneficial lease set-ups wherein entities lease a yacht to a nontaxable person or entity offer attractive fiscal proposals. The most adequate model for the particular situation depends on the specifications of the yacht and the intended use.

Country Highlights

| SOLUTION: Bespoke |

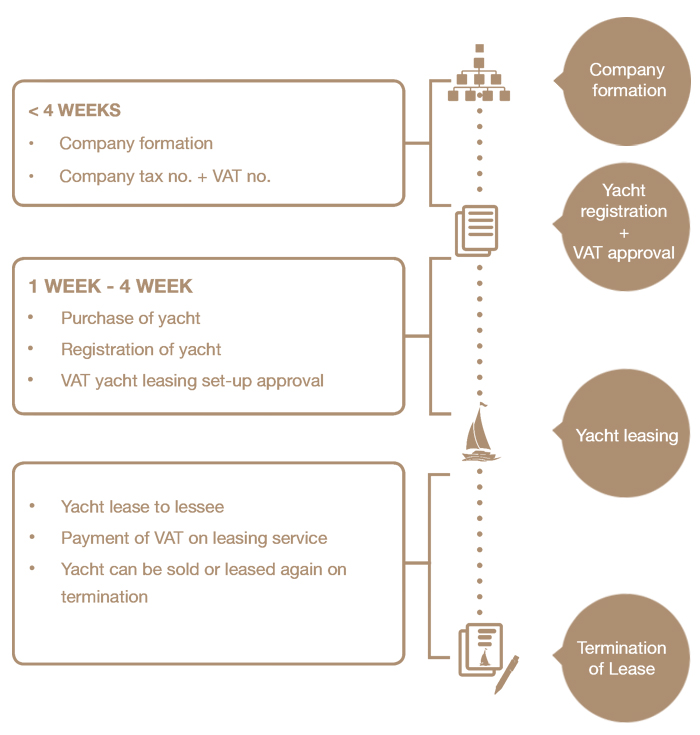

PROCESS TIMELINE: 4 – 8 weeks |

| EU ACCESS: Unlimited |

FLAG OF YACHT: Free choice |

| REPUTATION: European models |

YACHT LENGHT: No restriction |

Legal Basis

VAT treatment of yacht leasing is based on the rules emanating from the EU VAT Directive implemented with some variants within the EU member states. Different rates of VAT apply in the different EU member states, ranging from 17% in Luxembourg to 27% in Hungary. Notably, Malta has a VAT rate of 18%, being the lowest for port states. Whilst all EU member states are part of the VAT area (with some particular areas which are excluded), some non-EU countries are included, in particular, Monaco, which is included with France for the purposes of VAT. The applicable VAT rules in relation to VAT on yacht leasing distinguish between: short-term leases: the lease of a yacht for not more than 90 days; and long-term leases: the lease of a yacht for more than 90 days. The various rules apply depending on the yacht leasing model being assessed and the local implementation of the EU VAT directive in the applicable jurisdiction.

Benefits

- Tried and Tested Solutions

- Holding Entities: Asset Protection/Risk Segregation

- Costs: Relatively Low Establishment & Operating Fees

- EU & European Jurisdictions

- Complete structure & Yacht Registration within 8 weeks

Eligibility

- Lessor: a VAT Registered Entity in the Relevant Country

- Yacht: Purchased by Lessor Entity

- Approval of VAT Authorities

- Yacht leased to a Third Party

- Yacht Made at the Disposal of the Lessee in the Relevant Country

Process & Timeline

Why Work With Us